Ghost workers compensation insurance for contractors with no employees

You have no employees. You know you don’t need workers compensation. Then a general contractor calls and says you need a certificate of insurance showing workers comp coverage before they’ll let you on the job site.

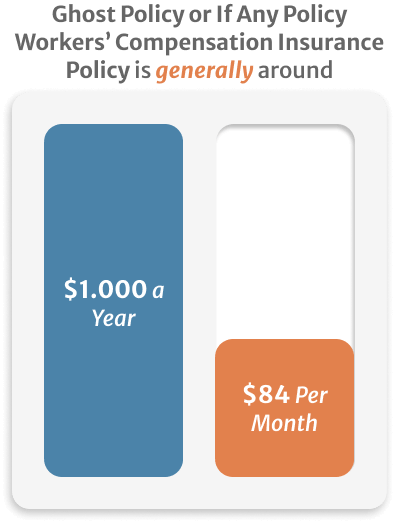

This happens dozens of times a day. It’s not a mistake, and it’s not negotiable. The solution is a ghost policy, also called an If Any policy. It costs about $1,000 per year, it satisfies the contractual requirement, and it keeps you working.

Get your Ghost Insurance Quotes Right Now!

Why the General Contractor is asking for this

When a general contractor’s workers compensation carrier does its annual audit, it asks for certificates of insurance from every subcontractor the GC paid that year. If the GC can’t produce those certificates, the money they paid those subs gets reclassified as wages. That amount gets added to the GC’s payroll and they get billed for the additional premium.

The math is straightforward. If they paid you $100,000 and you can’t produce your COI, that $100,000 becomes payroll. Their premium goes up significantly. To avoid that, they require every sub to carry workers compensation before work starts. No certificate, no job.

What a Ghost Policy actually is

A ghost policy, or If Any policy, is a workers compensation policy that covers you as the only person on it. There are no employees on the policy because you have none. The policy exists to satisfy the contractual requirement and give the GC the certificate they need. That’s its entire purpose.

It does not provide you with personal injury benefits the way a standard workers compensation policy would for an employee. What it does is keep you eligible for contracts with general contractors and larger clients who require proof of coverage.