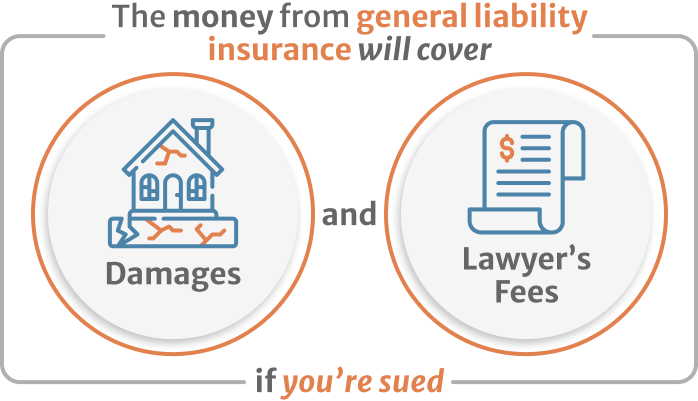

If you’re an independent contractor, you need to consider whether you should carry general liability insurance. This coverage is required by law in many states and industries. It is particularly essential if you’re working in a hazardous environment. The money from general liability insurance will cover damages and lawyer’s fees if you’re sued. In addition, independent contractors have the same legal obligations as big businesses. There are several reasons that a client or customer may decide to file a lawsuit. Without a general liability insurance policy, you could end up facing an expensive lawsuit and risk damaging your business’s reputation.

Independent contractors need this coverage because they’re vulnerable to lawsuits. In the digital age, even a 140-character Tweet can cause injury. Even if you’re not at fault, you can end up being sued if you make a mistake in performing a service or fail to deliver it. Fortunately, many commercial insurance brokerages can provide online quotes for contractors. If you’re unsure about the best plan for your business, NerdWallet’s ratings factor in customer satisfaction data and consumer complaints to help you choose a policy.

While general liability insurance isn’t a must for independent contractors, it’s a good idea. It protects your business from costly lawsuits for injury, property damage, and reputation damage. Moreover, many clients require independent contractors to carry general liability insurance. Independent contractors can purchase this insurance on the Internet or with an insurance agent. It’s important to keep in mind that the minimum amount of coverage for independent contractors is $2 million.

Continue Reading About Does public liability insurance cover employees

In addition to general liability insurance, independent contractors need to purchase insurance for their commercial vehicles. These policies cover the risks of accidents, damage to property, and equipment malfunction. Besides, a professional liability insurance policy will cover medical expenses if a 1099 contractor is found to have caused an accident on the job.

Independent contractors often use specific materials and equipment in the course of their work. In addition, if an independent contractor is working out of an office or retail space, they may need commercial auto insurance, which covers personal vehicles in the course of business. These policies will help cover damages to property, medical expenses, and lost income due to accidents. In addition, some independent contractors also have to carry business interruption insurance, which covers lost income and medical expenses due to a crash.

Whether or not an independent contractor should have general liability insurance depends on their contractual arrangement. While it may not be possible to cover work performed by a subcontractor, most businesses choose to carry general liability insurance for their subcontractors. It may save thousands of dollars. However, it is important to check the coverage for subcontractors and make sure that they are covered properly.

Aditional Info

If you’re an independent contractor, it is essential that you find an insurance company that can provide a variety of coverages to cover different types of projects. If you’re a sole contractor, you don’t need a large coverage, but you should make sure that you have enough coverage to cover the various tasks that you’ll need to complete. Also, check whether the insurance carrier will allow you to add additional insured endorsements and coverages. If you’re working on larger projects or have employees, you should consider purchasing a policy with a higher limit.

Having general liability insurance for independent contractors is an important investment that will protect your business from potential lawsuits. Even one lawsuit can derail your business. Without coverage, you may end up filing for bankruptcy. With liability insurance, you’ll avoid these risks and ensure your business meets all legal requirements.