Excavation Contractors Insurance

We have GREAT AUTO/HOME RATES!

Progressive Insurance

6300 Wilson Mills Rd, Mayfield Village, OH 44143

GEICO (Government Employees Insurance Company)

5260 Western Avenue, Chevy Chase, MD 20815

We cover all 50 States!

What is excavation contractor insurance?

Excavation work carries risks most other trades never face. You’re working around underground utilities you can’t see, in soil conditions that change without warning, with equipment that can kill someone if something goes wrong. A single utility strike can generate a claim that shuts down a small excavation business. A trench collapse on an occupied job site can be significantly worse.

Farmer Brown Insurance has been placing excavation contractors insurance across all 50 states since 1996. We work with A-rated carriers that write excavation regularly, including markets that other agencies cannot access. Same-day certificates. No COI fees.

Why excavation insurance is different from standard contractor coverage

Most general contractor insurance programs are not designed for excavation work. Standard general liability policies often exclude underground property damage, earth movement, and damage to utilities. An excavation contractor who buys a standard policy without confirming that those exclusions are removed or modified may think they are covered when they are not.

Farmer Brown specializes in excavation business insurance. We know which carriers write this class, which policy forms include underground coverage, and which exclusions need to be addressed before a job starts.

Type of excavation work we insure

We can provide Excavation Contractor Insurance for excavators who perform the following work plus many more:

- Excavation work

- Foundation digging

- Grading of land

- Dyke and Levee construction

- Soil erosion projects

Why do you need excavation contractors insurance?

Excavators are a vital part of many construction sites. Excavation at a job site can lead to many circumstances that can expose you to a considerable risk of loss. The only way to safeguard against huge financial losses in the event of an accident is through effective excavator insurance.

What insurance does an excavation contractor need?

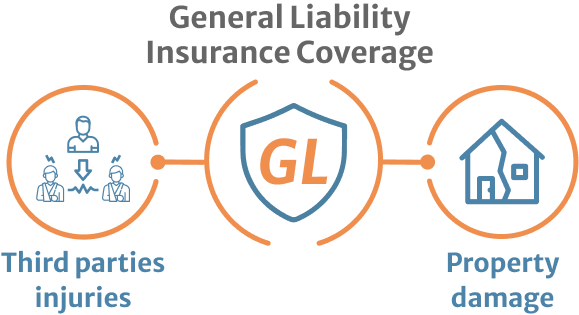

General liability insurance for excavation contractor

General liability, also called Commercial General Liability, covers third-party bodily injury and property damage. For excavation contractors, two components within general liability are especially important.

Underground property damage coverage. Standard general liability policies often exclude damage caused underground to pipes, cables, and conduits. Excavation contractors need a policy that specifically removes or modifies this exclusion. Hitting a gas line or a fiber optic trunk line without this coverage is a claim your policy will deny.

Completed operations coverage. If a problem with your grading or compaction work causes damage after the project is complete, completed operations picks up the claim. Foundation issues, drainage failures, and soil settlement problems often surface months after the job is finished.

General liability for small excavation contractors typically runs between $83 and $127 per month depending on revenue, location, and claims history.

Most general contractors require excavation subcontractors to carry at minimum $1,000,000 per occurrence and $2,000,000 aggregate, and to name them as additional insured for the duration of the project. No certificate, no access to the job site.

PRO TIP

If you hire subcontractors to help you out on a large project, you will want to have them name you as an additional insured on their policies. If you do not when your policy is audited the amount you paid them will not be deductible from your sales. The insurance company will treat them as uninsured subcontractors causing your Excavation Contractors Insurance premium to increase.

Umbrella insurance for excavation contractors

Given the severity of potential claims in excavation work, a commercial umbrella is worth considering. It extends your general liability limits when a claim exceeds your primary policy. A utility strike that damages a municipal water main or a trench collapse that injures multiple workers can generate claims that exceed a standard $1,000,000 per occurrence limit quickly.

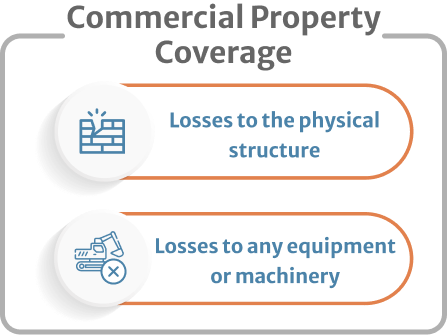

General liability insurance for excavation contractor

This type of coverage protects the property that your excavating, grading or earth moving business has if you operate out of a physical location. If you have a physical location you should have this coverage. It covers losses to the physical structure and any equipment or machinery stored there.

If a covered loss damages the structure or the machinery/equipment stored inside, your commercial property insurance policy would help to cover the cost of any necessary repairs or replacements. We all know the heavy equipment need to run an Excavation business is expensive. You need to make sure all your equipment has the right coverage. Without your equipment and/or the money to replace it you will be out of business in a hurry.

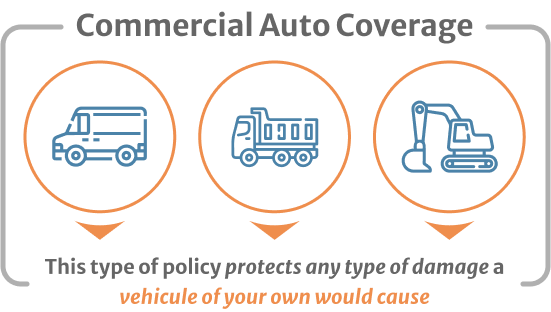

Commercial auto for excavation contractors

A loaded dump truck involved in an accident generates claims that personal auto carriers will decline. For contractors who regularly move equipment between job sites, this is not a policy to skip.

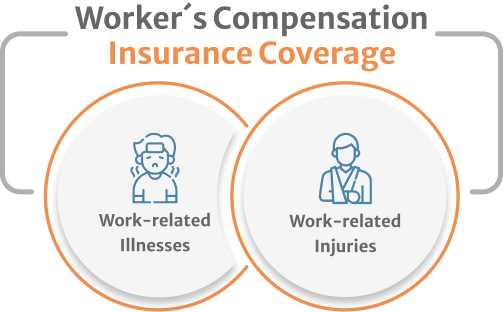

Workers compensation for excavation contractors

Workers compensation is required in every state except Texas for businesses with employees. Excavation work is physically demanding and genuinely dangerous. Trench collapses, equipment rollovers, struck-by incidents, and falls generate serious injuries. Workers compensation covers medical expenses, rehabilitation costs, and a portion of lost wages when an employee gets hurt on the job. When an employee accepts workers compensation benefits, they generally waive the right to sue the employer for that injury. That protection matters in a trade where injuries can be severe.

For excavation contractors, workers compensation rates are higher than most trades because the injury frequency and severity data for earthmoving work is worse than average. A clean safety record and documented safety training lower the experience modification factor over time and directly reduce the premium.

Inland marine for equipment

Excavation businesses run on expensive equipment. Excavators, bulldozers, skid steers, backhoes, graders, and compactors are routinely stolen from job sites or damaged during operations. Some contractors search for this coverage as heavy equipment insurance or excavator insurance. Whatever the label, the coverage works the same way: inland marine protects equipment wherever it goes, at the job site, in transit, or staged at a storage yard overnight.

Coverage is typically written at replacement cost rather than cash value. On equipment that depreciates quickly, replacement cost is worth having. Without inland marine, a stolen excavator comes out of your pocket.

Many municipalities and project owners require bonds before issuing permits or awarding contracts, particularly when the work involves public right-of-way or underground utilities.

License and permit bonds

License and permit bonds are required by many cities before issuing an excavation permit. The bond guarantees that the contractor will comply with licensing requirements and local regulations.

Payment and performance bonds

Payment and performance bonds are required by general contractors and property owners on larger projects. They guarantee that you will complete the contracted work and pay your subcontractors and suppliers. For bonds under $400,000, a credit score above 700 is typically sufficient. The standard rate is 1% to 3% of the contract amount.

PRO TIP

Add the bond cost to your original bid. If it wasn’t in the original specs and the owner asks for one after the fact, tell them before you lift a shovel. It’s easier to price it upfront than argue about it after.

How much does excavation contractors insurance cost in 2026

Excavation is a higher-risk trade than general contracting and insurance pricing reflects that. General liability for excavation contractors runs higher than the standard contractor rate because of the underground utility exposure and the severity of potential claims.

| Annual Revenue | Estimated Annual Premium |

|---|---|

| Under $150,000 | $1,500 to $3,000 minimum |

| $150,000 to $500,000 | $3,000 to $6,000 |

| $500,000 to $1,000,000 | $6,000 to $12,000 |

| $1,000,000 to $5,000,000 | $12,000 to $50,000 |

These figures are for general liability only. Workers compensation, commercial auto, inland marine, and bonds are priced separately and add significantly to the total program cost.

How do you get insurance policy?

Our primary goal at Farmer Brown is to provide you with the most cost-effective and comprehensive excavation insurance policy possible. We are well aware of the complex challenges contractors face when seeking excavator insurance to cover their business. Our mission at Farmer Brown is to provide you with a unique, targeted solution for your contracting business.

We offer a comprehensive range of insurance policies tailored to the excavation industry. We offer your business a choice from the high costs, poor coverage, and substandard service that is associated with many insurers. Our team consists of industry experts who can guarantee you the most prompt, efficient, and comprehensive service your Excavation Contracting business deserves.

Heavy equipment coverage for excavators

Excavation contractors depend on equipment that costs hundreds of thousands of dollars to replace. A single piece of equipment damaged by a trench collapse, a fire, or equipment malfunction can shut down a project and cost the business more than a year’s profit.

Operational risks include, but are not limited to:

- Equipment crashes/malfunctions.

- Fire.

- Rain damage.

- Lightning damage.

- Theft.

- Engine failure.

- And many more.

Heavy equipment coverage through inland marine addresses the specific operational risks excavation equipment faces: equipment crashes and rollovers, fire and lightning damage, rain and flood damage during extended site work, theft from unsupervised job sites, and in some policies engine failure and mechanical breakdown.

Equipment breakdown coverage is separate from inland marine and covers mechanical failure not caused by an external event. A hydraulic system failure on an excavator or a blown engine on a bulldozer would be covered under equipment breakdown but not under a standard inland marine policy. If your operations depend on specific pieces of equipment that cannot be replaced quickly, this coverage is worth pricing out.

Business interruption coverage. If equipment damage or theft forces you to shut down a project, business interruption coverage replaces lost income and covers ongoing fixed costs during the downtime. It is not automatically included in general liability or inland marine policies and requires a separate endorsement or policy.

Does my excavation policy covers lending and borrowing equipment?

Coverage for lent and borrowed equipment varies immensely between policies and insurance providers. If you are lending your own machinery, it is imperative that you confirm third-party liability is included in your heavy equipment insurance policy with your provider. It is not uncommon for third-party liability to be outside of a policy’s coverage limits; if you often lend heavy machinery to other contractors, purchasing an endorsement package will protect your equipment even if a non-employee is operating a machine during an accident.

If you are borrowing equipment from another contractor, it is equally important to confirm that the contractor who owns the equipment has third-party liability coverage with their heavy equipment insurance policy. Additionally, it is necessary to confirm the coverage of borrowed machinery under your own heavy equipment insurance policy if you have one. It is recommended to supply your own policy, even if all equipment used on a site is borrowed, to further protect yourself from paying for damages out of pocket.

Why Farmer Brown Insurance

Excavation is a hard class to place and most agents know it. We have placed coverage for excavation contractors for a long time and we know which carriers actually write it well, not just the ones that will take the application and add the exclusions back in. If you have been turned down elsewhere or got a policy that felt like it had more holes than coverage, that’s worth a second look.

We cover all 50 states, issue same-day certificates at no charge, and quote general liability, workers compensation, commercial auto, inland marine, and bonds together so you see the full picture before you commit.

If business interruption is not offered under those two policies, it may be provided with a heavy equipment insurance plan. Business interruption coverage is vital for covering labor costs and lost income if your team cannot operate for an extended period due to equipment malfunction.

Want to know everything about Contractors Insurance with updated information?

This E-book is for you!

Do you still have some questions?

Find us NOW!

We are located in 21750 Hardy Oak Blvd Ste. San Antonio, TX, 78258

Frequently Asked Questions

A place where you can find all the answers

Talk With An Agent Now

Let’s figure out how we can help you