Type of project

New construction and renovation are rated differently. A renovation on an occupied building costs more to insure than an empty lot. Projects with significant structural changes, like converting a warehouse into apartments or restoring a historic structure to current code, carry higher premiums than straightforward builds.

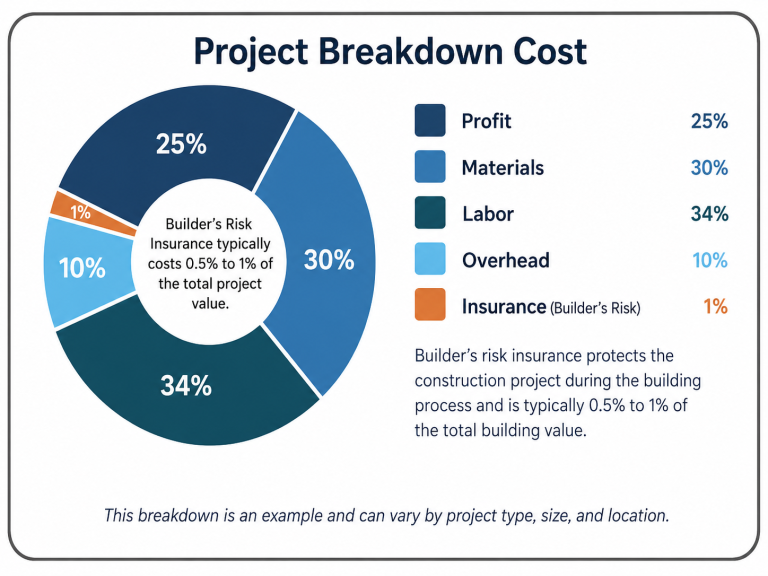

Construction Value

Higher value means higher premium. Custom materials, high-grade finishes, and complex mechanical installations all push the number up.

Location

Coastal properties, flood zones, and high-crime areas carry surcharges. Anything within 50 miles of the coast needs separate wind coverage that a standard policy won't include.

What you're covering

A basic policy covers fire, theft, vandalism, and wind. Adding earthquake, flood, off-site materials, soft costs, and debris removal increases the premium. Each one also protects against a category of loss that can easily exceed the cost of the extension on a large project.

Existing structures

A basic policy covers fire, theft, vandalism, and wind. Adding earthquake, flood, off-site materials, soft costs, and debris removal increases the premium. Each one also protects against a category of loss that can easily exceed the cost of the extension on a large project.

How far along the project is

Projects that are more than 30% complete at the time of application typically require additional underwriting. Get the policy in place before work starts.

Materials in transit

If materials are being stored off-site or are still in transit, you need coverage that follows them. That is an additional line on the policy and is worth including on any project where materials are staged away from the job site.

New Construction

The policy covers site preparation, excavation, foundations, framing, pipes, electrical work, and temporary structures. It starts with groundbreaking and ends when the certificate of occupancy is issued.

Renovation

Two structures are in play: the work being done and the building that was already there. A renovation policy can be written to cover only the new work or both the new work and the existing structure. If it is written to cover only the new work and a fire damages both the renovation and the existing building, you have a gap. That gap can be expensive.

Builders

Contractors

Retail Companies

School District

Find us NOW!

We are located in 21750 Hardy Oak Blvd Ste. San Antonio, TX, 78258

Frequently Asked Questions

A place where you can find all the answers

Talk With An Agent Now

Let’s figure out how we can help you