Insurance for Condominium Associations and Home Owners Associations

In a hurry?

Condo association insurance made easy

Buying a Master Condominium Insurance Policy is fairly easy. As a side note, Condominium Association Insurance will be used here as a blanket term used to describe many different types of community associations, such as co-ops, townhome associations, and HOA’s. For all these types of associations, there are 5 main coverages that every condo association should have.

There are also some extra endorsements you can buy for an additional premium. This is just meant to be a very simple explanation of coverages.

Please feel free to give us a quick call for a more in-depth review of the policy your particular association needs.

KEEP READING BELOW FOR INDUSTRY INSIDER TIPS!!!

The policy you will buy is called a Business Owners Package or BOP policy. These policies automatically include a package of coverages that is standard for the average condo association. Policies are easy to write. There are companies that specialize in Condominium Association Insurance and can have a policy bound very quickly for smaller associations.

Most of the coverages are standard in Condo association Insurance. Further, most states have laws setting out the minimum coverages you are required to have.

Getting a quote from top condominium insurance companies is as easy as:

"*" indicates required fields

Our proprietary program will calculate the coverage you need. We will generate a ballpark estimate of a rate. If our rate looks good we will contact you and firm up the quote. We will also see if you want any additional coverage. We find that in 7 out of 10 cases we can offer you a policy with similar coverage for less money.

Condo association insurance is designed for:

- Homeowners associations.

- Secondary associations.

- Seasonal associations.

- Timeshare associations.

The most important coverages in buying a Master Insurance Policy:

1.Property Coverage

It is important that you purchase enough coverage to replace your building. The replacement cost of your building is not the market value of all of the units added together, but the amount it costs to rebuild your building. Our agency provides you with a free replacement cost analysis, or you can go to Marshal & Swift to do your own in a few steps.

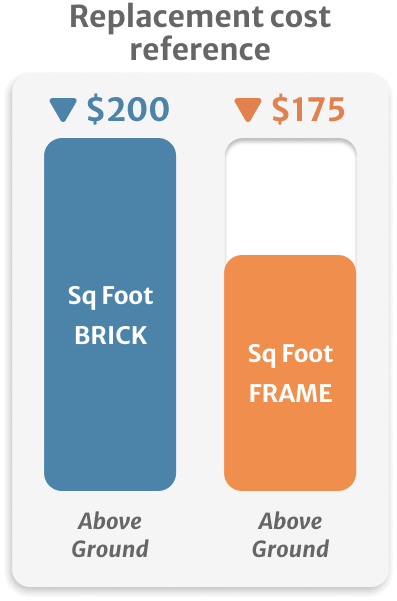

A pretty quick reference is that your building should be insured for about $200 per square foot above ground for brick construction and $175 per square foot for frame construction. If you are in more of a simple building or in a state where construction costs are lower, it certainly could be less. If you are in a state with higher construction costs such as California or New York, it could be more. Also, if you are in a very high-end building, it could go much higher.

“Walls Out” means that the insurance for the association covers the building structures, up to the uncovered drywall and sub-floor. They do not insure the paint on the walls, the carpet on the floors, or interior fixtures such as cabinets, toilets, and countertops.

“Walls-in” Means that the association’s master policy provides coverage for paint, carpet, and cabinets. Most governing documents requiring this type of coverage state that, in the event of a loss, the insurance for the association should pay to replace the unit back to its condition as it was originally built. If there have been upgrades made since then, such as a remodeled kitchen with a high-end build-out or the original flooring has been upgraded, the condominium owner would have to cover this replacement from their own pocket. To protect against this the unit owner would need to purchase their own policy (called an HO6 policy).

2. General Liability Coverage

It is standard to have general liability coverage at $1,000,000 per occurrence and $2,000,000 Aggregate. This means if there is a general liability claim against your building (usually for slip and fall) you have $1,000,000 per incident with a maximum of $2,000,000 per year in total.

3. Fidelity Bond/Employee Dishonesty

This coverage protects the association if the manager or one of the board members steals the money in the bank. You should have the amount of your reserve bank account and your operating bank account added together for your coverage. This coverage is very inexpensive.

4. Directors & Officers Liability Coverage

This coverage protects you from being sued by your condo association for making a decision that adversely affects your condominium association. This coverage is a must unless you are in an association 4 units or less and everyone is on the board. One of the most important features of this is that it covers attorney fees that are required to defend the association and board members.

5. Building Ordinance Coverage

This coverage covers you to rebuild up to code and can be very important if you are in an older building and there have been code changes over the years. This is most important if your building in the future will be required to rebuild with sprinklers.

WARNING

Did You Know?

You will need to buy a separate condo owner’s policy or HO-6 policy in insurance lingo. This protects your personal property. Your personal property is your furniture, electronics, clothing, and other movable property you have in the unit.Your HO-6 should also provide general liability coverage and other coverages, such as loss of use, if for some reason you are unable to inhabit the condo and need to find a temporary place to live. None of these items are included in the master policy.

Extra coverages

There are also extra coverages you should buy if you need them depending on your building and the part of the country you live in. Below are the coverages you should look into:

Sewer Back-Up Coverage

If you have a building with a basement, it is important to have this if the sewers overflow.

Flood Coverage

This is required by law for your building to have if your building is in a flood zone. This is different than sewer backup, for flood insurance only covers damage that comes from a body of water.

Earthquake Coverage

If you are in an area prone to earthquakes, you should have this coverage.

Extended Replacement Cost

This is a great coverage to have for it gives you a 10% to 25% buffer if your building has a total loss and you did not purchase enough property coverage.

Business Personal Property

This is covers everything not attached to the building that the association owns. This could cover items such as snow blowers and lawnmowers that an association might own. Most smaller associations do not own much significant property and usually, this can be self-insured.

This is clearly a simple overview of coverages, but hopefully opens up some things to consider in purchasing your Master Association Policy. Please feel free to call us at any time or fill in the simple form above for more information. Thank you for your consideration and we hope you found the quick information helpful.

How much does condominium association iInsurance cost

For a small Condominium Association, the costs range about $97 per month. This is obviously only a general estimate. The major factors determining the cost of Condominium Association Insurance are:

Size of association

This is straight forward. An Association that has 500 units will pay more than an Association with 4 units.

Type of construction

Frame construction is more expensive to insure than masonry noncombustible construction that has proper fire divisions.

Loss history

If the Association has had claims in the past, the premiums will be higher.

Location of property

Where the property is located has a great impact on cost. For example an Association located on the coast that is hit with seasonal storms will pay more than Associations located away from the coast.

PRO TIP

Be aware of your deductibles when shopping for Condo Association Insurance. I have a horror story to relate to this point. We had an association that had their insurance with us for a number of years. They had a $5,000 deductible with us. They went with another agency that offered a policy that was $3,000 less but had a 10% wind and hail deductible. 3 months into the new policy a severe hail storm struck the area. The association buildings suffered in excess of $2.5 million in damage. This meant that the Association had to come up with over $250,000 from their reserves to cover the deductible. So the $3,000 premium savings cost them $250,000 in the long run.

Association’s insurance vs homeowners and condo insurance

A condo association insurance policy usually includes coverage for accidents and injuries that happen within the complex’s common grounds. Furthermore, a building’s exterior damage is normally under the association’s property damage coverage. Associations also have coverage for commonly owned personal and affixed property such as a tool shed. On the other hand, individual unit owners must be insured against damages and accidents that might happen in their units. If wallpaper in their living room rips off, the individual policy will cover the repair.

It is important to remember that the personal property of the individual unit owners is not covered under the master association policy. Personal property is furniture, clothing, electronics, and similar items located in individual units. There is also no coverage under the Condominium Association Insurance policy if someone is injured in your unit. With both homeowners and condo insurance, you will need to ensure you have enough coverage to protect the value of your personal belongings and against any claims for personal injury.

WARNING

Remember, if you do something that causes damage to another person’s unit, such as you accidentally let your bathtub overflow, for example, this will not be covered under the Condo Association Insurance policy. If you do not have your own condo insurance policy, you may be stuck paying for repairs out of your own pocket. In other words, Condo association insurance coverage is usually limited to building exteriors and common areas such as parking lots, while a personal condo owner’s insurance must insure against injuries and property damages done in his or her unit.

Frequently Asked Questions:

What Is A Condo Association or HOA?

A Homeowners Association or Condo Association is an organization or community development to which members pay fees for certain services. As a home or condo owner, you are automatically part of the Association. As a result of being part of the association, you subject to certain rules and regulations set forth in the by-laws. These by-laws are generally enforced by an elected board chosen from the members of the association.

HOAs often have rules for how you maintain your home. These range from trivial matters such as not allowing decorations on doors and balconies to the ability to vote in special assessments to fund capital improvements.

When you pay your HOA dues, that money is used to cover maintenance, improvements, and HOA insurance, which is also known as your community’s master policy.

What Is Condominium Association Insurance and HOA Insurance?

If you own a Condominium, Co-Op, or live in an HOA with single family houses or townhomes, you typically need pay for two types of property insurance. These are individual home or condo insurance and a master HOA insurance policy.

As you know you are required to show your mortgage company proof of insurance if you have a loan. If you live in a condominium or other type of property in an HOA you will also have to pay for your portion of the insurance on the common areas. Your monthly assessment pays for the community’s HOA insurance. This is often referred to as the association’s master policy. It protects the association’s communal property if it is damaged along with providing coverage if people are injured in the common areas.

What is Walls-In Coverage?

Wall-in coverage means that the Association covers the interior fixtures of your unit. Typically, items such as basic flooring, cabinetry, plumbing, and electrical fixtures are included in the Condominium Association’s insurance policy. It is important to realize that this usually only means builder-grade finishes. If you have high-end flooring, cabinets, and appliances these will not be replaced by the master policy. It will only cover the cost of basic fixtures.

What is Walls-Out Coverage?

This term means that the Condominium Association Insurance is covering the structure of your residence. It only covers up to the drywall. All other items such as flooring, plumbing, and electrical fixtures, cabinetry, and appliances must be added to your individual Homeowner’s policy.

Can my Condo Association Insurance Cover Hurricane Damages?

If you have the “all in” policy, then the answer is yes. Your condo association insurance policy will cover the damages to your property and the interior of your condo building by major storms like hurricanes, tornadoes and windstorms. This can also cover the plumbing, wiring, and other repairs.

If you only have the “bare walls in” policy on your condo association insurance then you will need to talk to your insurance agent to ask for an additional policy for your condo association insurance. It is always important to have everything covered by your condo association insurance to avoid any coverage gaps and to avoid financial losses.

How much coverage do I need?

You need to know which areas or parts of the condo unit you must get insured, and you need to decide and plan how much coverage you need. You can draw an estimated coverage by basing it on how much owners are in the complex and who paid for upgrades or remodeling such as changing the roof, flooring, and a lot more.

Want to know everything about Contractors Insurance with updated information?

This E-book is for you!

Do you still have some questions?

Find us NOW!

We are located in 21750 Hardy Oak Blvd Ste. San Antonio, TX, 78258

Frequently Asked Questions

A place where you can find all the answers

Talk With An Agent Now

Let’s figure out how we can help you