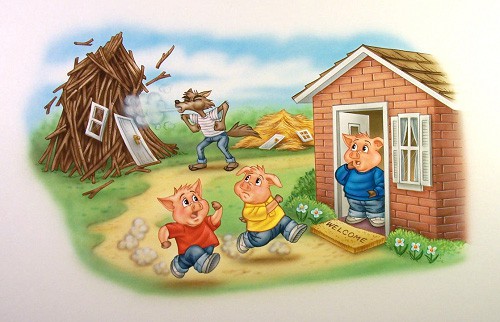

Everyone knows the story of the 3 little pigs. One pig built a house of straw while the second pig built his house with sticks. They built their houses very quickly and then sang and danced all day because they were lazy. The third little pig worked hard all day and built his house with bricks. A big bad wolf saw the two little pigs while they danced and played and thought, “What juicy tender meals they will make!”. This situation is analogous to the three different coverage options you can choose with vacant building insurance. They all offer some level of protection from The big bad wolf of claims.

In deciding what type of policy to pick it is important to know about is called “co-insurance penalty”. This is a penalty for not insuring your building to 80% of the rebuilding cost which is determined by Marshal & Swift (a company that specializing in labor and material costs in the construction industry). Replacement cost is based on square footage and a cost per square foot to rebuild. Reconstruction costs can range from $90 per foot to $500 per foot for super high end construction which would be rare in most vacant home policies. For this example, lets say the pig’s house is 3000 square feet and reconstruction costs are $100/foot. Mr. Pig would be required to insure his house to a minimum of $240,000. ($300,000 reconstruction cost *.80). If Mr. pig insures his building to less then $240,000 he will be incurring a penalty using the following calculation:

amount of coverage purchased/replacement cost *.80.

If Mr. Pig had his house insured to $120,000 the equation would look like this:

$120,000/$240,000($300,000*.80)=50% paid on total claim

This is extremely important you know how much building coverage you should purchase for the wrong amount of coverage can really come back to sting you. First, you need to understand that you insure your building to the amount that it costs to rebuild. You do not insure it to market value for the land can’t burn. That being said there are two types of insurance you can buy and they have to do with how a claim is settled. The first is called “actual cash value” coverage and gives you the actual cash value of the damaged property from a covered claim. The second is “replacement cost” coverages and pays to rebuild your building with new materials. Below is an example of how a claim would be handled with both types of settlement provisions:

Mr. Pig’s home was damaged from the big bad wolf and was insured to $300,000 of building coverage and his home was built in 1980. Mr. Pig suffered $100,000 in building damage to repair with new materials and has a $2500 deductible. Below are the settlement scenarios from the insurance company:

- Actual Cash Value Coverage: This is the straw house. The claims adjuster has determined there has been 50% depreciation on the building since being built in 1980. Pig would receive $47,500 for his claim. This comes from $100,000 in damage being depreciated to $50,000 (50%) and subtracting his $2500 deductible. If the straw house pig was really lazy it gets worse… If Mr. Pig has Actual Cash value they will depreciate first before the coinsurance penalty.So here is where we will be at: $100,000 claim after co-insurance penalty will bring the payout to $50,000. Now 50% depreciation from ACV settlement provision. Which brings payout to $25,000. We then subtract $2500 deductible which brings us to a payout of $22,500.

This could be a disaster for Mr. Pig if he does not have the money to fix for he cannot borrow from the bank on a vacant building. As in anything else, with vacant building insurance you get what you pay for.

- Replacement cost coverage: Mr. Pig in the stick house would receive $97,500 from the insurance company to replace the Wolf damaged portion of his building.

As you can see the difference in settlement provisions can have a huge effect on the total payout on the claim. Actual Cash Value is usually about a 30% savings in premium and you can make the determination if the savings is worth the cost in the event of a large claim.

The strongest house or policy is the replacement cost policy with the building insured to 80% of replacement cost. This policy will cost the most but will protect you the best if the big bad wolf tried to huff and puff and blow the house down.

What Is Definition of Vacancy?

Next you have to determine what is considered a vacant building. Generally speaking, if the home can be lived in meaning there is cooking equipment, tables, chairs, working bathrooms the home can be considered “unoccupied”. If there are only some books and a couch, there is precedence that the home is vacant.

It is extremely important to know if your home is “vacant” or “unoccupied” for if it is vacant for more than 30-60 days, you will lose your theft and vandalism coverage. This is obviously hugely important for they are the most common claims. Most policies take away theft and vandalism after 30-60 days of “vacancy” leaving only coverages for fire and vandalism.

What if I am renovating my home?

If your home is under renovation and no one is sleeping there, it will probably be considered vacant after 30-60 days and therefore coverage only for fire and liability.

If my home is being renovated, are construction materials covered?

This is covered as an additional endorsement on most vacant home insurance policies. You have to state the amount of renovations and coverage is added on.

How long are the policy periods I can choose to purchase?

You can purchase a 3 month, 6 month or 12-month policy. If the period comes up for renewal and the structure is still vacant you can renew a policy for the same time period or a different time period if you choose.

If the home becomes occupied again, can I cancel the policy and start homeowners’ policy?

You can cancel the policy; however, the policies are considered “one shot” policies usually and there is not return in premium for not making it through the policy.

Am I covered for wind/hail in the event of a claim?

This depends on the state you are living in. Some policies cover this and some do not. Generally speaking, if your home is in a coastal area there is not coverage for wind/hail and it needs to be purchased through the state fund

Am I covered for water damage from a frozen pipe if the home is considered vacant?

The answer is usually “no” and this is the most common claim. A person goes to Florida for winter and while they are gone, a pipe bursts from being frozen. This claim can be covered if the home is “unoccupied” and not vacant; otherwise, there is no coverage.

These are some ideas to think about when purchasing a vacant home policy. The most important idea is that not making a decision is making a decision when deciding to change your insurance from an “occupied” home to a “vacant” home. Plan ahead and put yourself in the position of the insurance company. In the event of a claim, they will go by policy language in the application that you signed. A large uninsured claim can be a financial disaster that can be avoided by thinking ahead and paying a few extra dollars.

If you need somebody to explain these choices further feel free to reach out to me. I have over 20 years experience in helping Small contractors and am the owner of one of the largest internet providers of all types of insurance for contractors on the internet. I can be reached at (888) 973-0016 or by Email [email protected].