Handling insurance aspects of any kind is a complex task. Learning the ins and outs of business insurance for general contractors is no exception. These types of policies must account for potential costs like accidents and injuries on the job, and weather-related damages – to name only a few.

Business Insurance Rates

Choosing the right insurance coverage for your business can be a daunting task, especially when trying to understand the different types of insurance and their varying rates and limits.

To help you make informed decisions, we have compiled a comprehensive table of insurance types, median policy rates, per claim and policy limits, and median policy deductibles.

Keep in mind that actual rates and limits may vary depending on a range of factors, but this table serves as a useful starting point for estimating costs and understanding the key metrics of each insurance type.

|

Type of Insurance |

Median Policy Premium |

Per Claim Limit |

Median Policy Limit |

Policy Limit |

Median Policy Deductible |

|

General Liability Insurance |

$380-$1,380 |

$1,000,000 |

— |

$2,000,000 |

$1,000 |

|

Business Owner’s Policy |

$500-$639 |

$1,000,000 |

— |

$2,000,000 |

$500 |

|

Surety Bond |

$100-$300 |

— |

Varies |

— |

Varies |

|

Inland Marine Insurance |

$500-$759 |

— |

Varies |

— |

None |

|

Commercial Auto Insurance |

$1,854-$2,846 |

— |

$1,000,000 |

— |

$500 |

|

Umbrella Insurance |

$1,010-$2,020 |

— |

$1,000,000 |

— |

Varies |

|

Worker’s Compensation |

$5,723 – $7,656 |

$100,000 |

$500,000 |

— |

None |

|

Commercial Property Insurance |

$253 – $1,630 |

— |

Varies |

— |

$500 |

Types of Insurance for General Contractors

Business insurance is usually not an all-in-one package. Therefore, figuring out what type of insurance your company needs is a process best completed with the help of a policy provider. Here are some of the common insurance types for artisan contractors.

General Liability Insurance

Accidents happen. General liability insurance exists specifically for this problem. It’s what covers you when your plumbers accidentally put a hole in a wall or if a client believes your work isn’t up to par.

This type of insurance covers any sort of lawsuit that arises from workplace negligence, property damage, injury, and/or disputes over your work. Most contractors do have some form of liability insurance, for legal reasons as well as ensuring their own security.

Property Insurance

Let’s say someone comes on to a worksite and vandalizes some of your vehicles. Or, perhaps company tools were stolen from a workplace. Property insurance handles these types of claims. While it’s not necessary for a general contracting company to have this type of insurance, many companies do.

Business Owner’s Policy

Do you want to bundle the two insurance plans already mentioned? A business owner’s policy can do just that. In general, these policies cost more than the average policy for a general contractor, but it saves more money than paying for two separate general liability and property insurance policies.

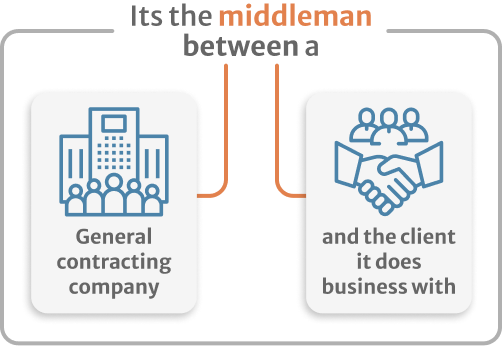

Surety Bond

Think of surety bonds as the middleman between a general contracting company and the client it does business with. Purchasing this bond through an insurance company shows state and federal governments that you are committed to complying with their laws. Contractors purchase these when they apply for a license or a building permit, as they are required by law in almost every state.

Nonetheless, it is worthwhile to understand how much a surety bond will cost. Deductibles and policy limits vary greatly, so make sure to go over those limits with your insurance agency.

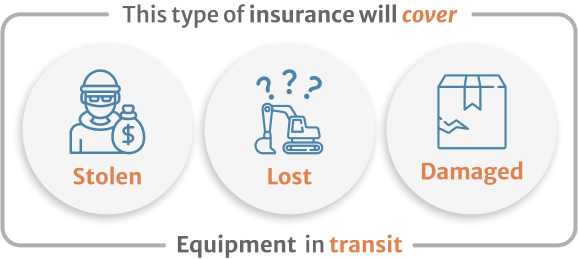

Inland Marine Insurance

Don’t let the name fool you – it has nothing to do with the ocean, at least today. This type of insurance was one of the earliest types of insurance, back when equipment was shipped overseas by boat. Today, this type of insurance deals with contractors who work solely to haul equipment from job site to job site. If equipment is stolen, lost, or damaged in transit, this type of insurance will cover the losses.

Commercial Auto Insurance

Did you know that most personal car insurance policies do not cover injuries or damage, even while at work? This is what commercial auto insurance is for. It ensures that drivers and vehicles are covered, regardless of who they belong to. Driving is a big risk, no matter where you are or where you’re headed. The number of situations that may occur on the road are things many drivers employed by general contractors are looking to be covered for.

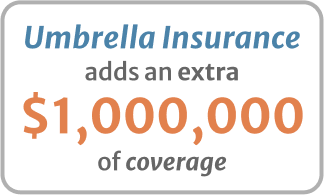

Umbrella Insurance

You might be wondering what happens after a claim reaches the policy limit. General contract prices can be high, after all. If you’re a larger company and you’re afraid that the policy limit for your general liability insurance, hired auto insurance, non-owned auto insurance, and employer’s liability is too low, umbrella insurance adds an extra $1,000,000 of coverage to a claim covered by one of these insurance types.

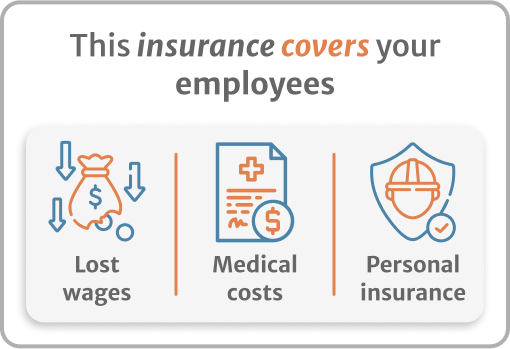

Worker’s Compensation

Everyone has heard of “worker’s comp”, but how does compensation work, exactly? For general contractors, this type of insurance covers medical costs, lost wages, and personal insurance for employees injured on the job. This is one of those types of insurances that every business will need, but a hands-on business like a general contractor’s company would especially consider worker’s comp to be a vital investment. Not only is it best to have this type of insurance in case of injury, but in most cases, it is required by law.

Commercial Property Insurance

This type of insurance covers loss or damage to a general contractor’s equipment. Typically, there are exclusions on this. Most commonly, the types of damage covered include certain weather events, theft, vandalism, and fire. The types of events covered in your area can differ greatly from another area, as is the case with nearly every other insurance policy. For instance, a gulf coast construction business might not have coverage for wind-related damages, but a business in another place that is not prone to a lot of wind might include wind in their coverage.

Understanding Insurance Terminology and Key Metrics

Here we will include a few definitions of general terminology, as well as generic rates for each, for estimation purposes. Actual rates will vary, and good policy providers are more than willing to explain those variances to you when you sign up for your free quote. All rates shown below are in USD. When applying for your personal policy, be sure to ask about annual, bi-annual, or monthly rate options, as many have annual-only premium payments.

-

Policy Premium:

The amount of money a business pays to have an insurance policy.

-

Median Policy Premium:

This represents the average or standard deviation of a policy premium. When median policies are listed there is a chance that they could be higher or lower, based on a variety of factors.

-

Per Claim Limit:

This is the highest amount of money that can be paid when an accident is reported.

-

Policy Limit:

This is the maximum amount of money that your insurance company will pay you for an insured event.

-

Median Policy Limit:

This is the middle ground, or average, representation of a policy limit. This means that an individual policy limit could be higher or lower than the listed limit.

-

Policy Deductible:

A deductible is the amount of money that the policyholder will pay out of pocket before the insurance company will assist with payment.

-

Median Policy Deductible:

This number represents the average or standard deviation amount of a policy deductible.