As a General Contractor, you confront risky deals everyday. Your employee’s can get hurt, your clients property can get destroyed and you can get sued!

Don’t take your business too lightly. Find out how you can protect yourself and your business from hefty labilities. Here are two key reasons why general contractors get sued:

Do you want to avoid those risks??

Get a free quote for your General Liability Insurance Now!

1. Breach of Contract

The typical causes of action from a building construction contract against a licensed building contractor are breach of contract for the contractor’s failure to respect the terms and conditions. This can include:

- Breach of implied and express guaranties of fitness.

- A petition to remove an unnecessary lien for defects with the recorded contractor’s lien on the property.

- Carelessness for the contractor’s work not meeting up with industry expectations.

- Strict debts for substandard construction regardless of the contractor’s valid reason.

- Fraudulent activity from the contractor’s misrepresentations to the property owner.

- Indemnity for the money the general contractor owes to his subcontractors.

Additionally, if a person is seriously injured through substandard construction by the contractor or subcontractor, a property owner could bring a personal injury cause of action for negligence or strict liability for defective construction. Contractors Liability Insurance can protect against such a case.

Construction defect occurrences are tough and require specialists to prove a homeowner’s claim against the person carrying out the work of development which was improperly done. Given the requirement for experts at trial and the complicated nature of a construction defect case in which destructive testing ( setting up walls of a home for instance ) is needed, and proving the failure of the work is not meeting industry expectations or present building code or rules, a qualified lawyer in this field is a must.

There are so many rules and ways you can violate a contract. If you are a general contractor you can protect yourself with General Contractors Insurance.

2. Employer vs. Employee Conflicts

Many workers quit and then sue their bosses, as a result of a lack of clarity of what exactly is expected from the worker. Workers seek legal guidelines when the hours, the pay, the tasks, or other conditions are not clear. They apparently really feel exploited when the scope of their responsibilities surpasses the standards that were established during the orientation.

Companies need to be very clear as to what exactly is expected of workers from the very beginning when the job relationship is established. For some reason or other workers usually feel mistreated whenever their specifications and actual responsibilities are conflicting.

Employee’s quitting or thinking of laying off usually seek legal advice once they feel they have been mistreated, and even though there might not be a basis for a legal action on the grounds that the worker feels mistreated, an expert lawyer knows what questions to ask and a lawsuit might result.

Some Common Employer/Employee Conflicts Include:

- Terminating any worker who takes a leave of absence.

- Implementing a “use it or lose it” vacation policy and also avoid paying out all the money at end of contract.

- Inherently Dangerous Work.

To protect yourself from these employer-employee conflicts,

Get a Worker’s Compensation Insurance, Now!

How General Contractors Can Protect Themselves from a Lawsuit?

With all the complexities of business law and finances, be sure to follow the following steps to protect your business from legal action and financial loss.

- Trademark Infringement Lawsuits.

- Separate Yourself from Your Business.

- Appoint a Competent Attorney.

- Protect and Secure Your Business Files.

- Get Business Contractors Insurance.

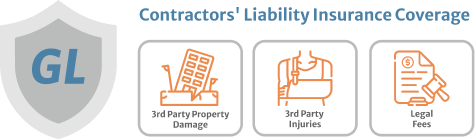

Essentially, Contractor’s Liability Insurance provides protection to the business proprietor against problems that can arise from a lawsuit against his or her company. To start with, insurance covers damages should they be awarded to a third party over possible injuries or damages in which the contractor has been deemed responsible.

This consists of loss of property claims. However, liability insurance will take care of the expense of lawyer fees, investigation costs, court fees as well as other legal expenses entailed during the course of litigation, should any occur.

Thinking about how fast, and how high, these kind of expenses can add up, a contractor working without insurance plan could easily end up in bankruptcy court simply to settle up the legal charges.

The hard truth is, in fact, that these types of fees can increase even in cases by which it is eventually decided that the contractor and his or her enterprise are in no way at fault.

Both of these factors are the two important elements of any contractor’s liability insurance policy. Basically, those two elements cover both payment of damages on the insured’s behalf and all legal charges arising from the lawsuit and subsequent defense against it.

A contractor might find himself on the business end of a lawsuit for any number of factors, but most occur from one of three broad classes of “legal wrongs.” These are 1 crime, 2 breach of contract, and 3 tort. All these are dealt with by various branches of the law.

- Crime

- Breach of Contract

- Tort

Criminal acts on the part of the contractor might also play a role in civil cases further along in the legal procedure. Financial rewards are usually given as remedies. A typical illustration of this would be fraud, for example, in which a contractor willingly defrauds a client. While fraud involves criminal liability, this also can be addressed in civil court whereby the victim may sue for monetary damages.

When it comes to these civil suits, the victim might sue not just for monetary damages, but also for such esoteric, non-monetary reasons as punitive damages for emotional distress. In many courts, it’s very easy for the costs for the contractor to accumulate all too quickly.

Without liability insurance, a company owner can easily see an enterprise he or she has developed over the course of several years go down in just a few weeks.

You need insurance to protect your business assets. Get a 5 minute quote or contact us today to get the best rates and coverage for your needs.