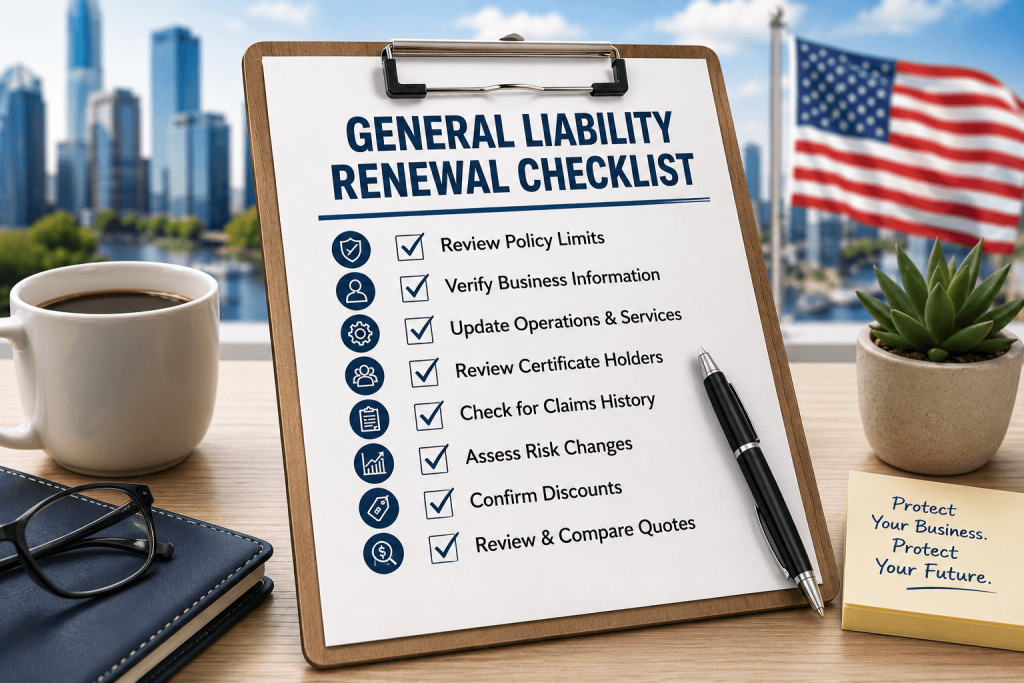

General Liability Renewal Checklist

Renewing a general liability policy is not a formality. It is the right moment to fix coverage gaps, update information that affects your premiums, and make sure the policy still fits how the business actually operates.

Farmer Brown works with contractors across all 50 states on exactly this kind of review. Here is what to go through before signing off on another year.

Verify your payroll numbers before renewal

GL premiums for contractors are tied directly to payroll figures. If the numbers provided at renewal are off, an end-of-year audit catches the difference, and the additional premium comes due, then usually in a lump sum.

Pull current payroll records before the renewal meeting. If headcount or total wages have shifted significantly since the last policy period, that needs to be part of the conversation.

Read the exclusions before the policy renews

Every policy has them. The ones that matter are the ones that touch the work you actually do.

Read through the exclusions before renewing. A policy that carves out a risk category central to your projects is not real coverage, regardless of the premium. The worst time to find an exclusion is after a claim is already filed.

Check whether client contracts require specific coverage terms

Some clients require specific endorsements, coverage terms, or additional insured status before a contract is signed. Those requirements have to reach your insurance agent before renewal, not after.

A legal agreement between you and a client that was never disclosed to the insurer may not be covered under the policy. Bring the contract language to your agent and confirm the policy accommodates it before you commit.

Collect current certificates of insurance from every subcontractor

Get current certificates from every subcontractor before renewal. Without them, carriers may treat money paid to subs as part of your payroll when calculating what you owe. That number goes up fast.

Current certificates from properly insured subcontractors keep those costs where they belong.

Confirm subcontractors carry their own workers compensation

A GL policy does not cover employee injuries on the job. That gap matters more than most contractors realize until it is not covered.

If a sub’s employee gets hurt and that sub carries no workers compensation, the liability can land on you. Request documentation from every subcontractor before work starts, not after something happens.

Disclose potential claims before the renewal is finalized

If there is an incident or situation from the current policy period that could produce a claim, tell your agent before the renewal closes. Getting ahead of a potential claim is simpler and less expensive than having it surface mid-policy when options are limited.

Response time is a sign worth paying attention to

One practical sign that an agent is worth keeping: they return calls and emails the same day. Coverage questions during an active policy period do not wait, and agents who go quiet at renewal tend to stay quiet when claims need to be managed.

Farmer Brown’s team responds within one business day and handles general liability coverage for contractors across all 50 states. If the current policy no longer fits the operation, a second opinion before signing costs nothing.