Find the Best Rate for Your Surety Bond

Managing the risks on your construction projects and choosing the best option to ensure that your project gets done on time is very important to running a successful business. When this is not taken seriously, you can go bankrupt, especially when dealing with a contractor or subcontractor unsure about their commitments.

Surety bonds give you the solution to those problems: providing financial security, ensuring that contractors will finish the work and pay the laborers, suppliers, and subcontractors, and giving the project owners relief and protection. Let’s look at the most important things to know about surety bonds:

Surety Bond Definition

Surety bonds for a construction project or business are known as contract surety bonds. They are a three-party contractual agreement where the surety (the party that guarantees the debt) guarantees the obligee (the project owner) that the principal (the contractor) can carry out the contract in accordance with the contract documents. To sum up, Surety bonds assure the business owner that the contractor will follow through on the contract.

Types of surety bonds

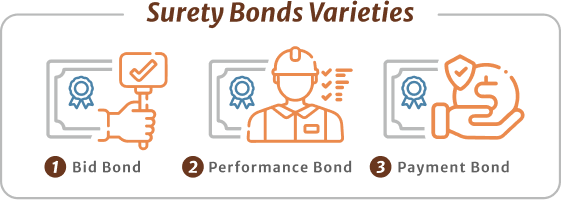

Contract surety bonds come in three varieties:

- The first is the Bid Bonds, which give financial security. It ensures that the bid has been submitted, and the contractor will render the required performance and payment bonds.

- The next one is the Performance Bond, which protects the business owner from risks, specifically financial loss, when the contractor does not meet the contract’s requirements.

- Lastly, the Payment Bond gives the security that the contractor will pay their workers, suppliers, and others they hired for the project.

Difference between Surety Bonds and Standard Insurance Policies

Surety companies are under insurance companies, so both surety bonds and standard insurance policies are risk transfer mechanisms implemented by the state insurance departments. The only difference is that traditional insurance is made for the compensation of the insured in case of unwanted events or accidents, and companies that offer surety bonds operate differently. Surety bonds are made to prevent losses, stabilizing the contractors through financial strength and their skills and expertise.

The Law

The US Government requires contractors to get surety bonds to assure that they will do what’s stated in their contract and pay those they hired for the project. This law, called the Miller Act, requires contractors to have two bonds on contracts worth more than $100,000.

Benefits of Contract Surety Bonds

Construction projects are usually full of risks. Thousands of contractors don’t last long; According to KPMG, 53% suffered one or more underperforming projects in 2014. More recently, 64% of construction businesses reported not being prepared for the effects of the pandemic in 2021, and even the ones that were prepared suffered from project delays and financial implications. Surety bonds guarantee that contractors will be able to complete their projects on time and keep all costs within the budget.

- Having a surety bond will provide the business owner the peace that a risk transfer mechanism is in place, and the liability from the construction risks is now in the hands of the surety company.

- During the evaluation process, contractors are judged on their abilities to meet the agreements on the contract.

- Contractors usually tend to finish projects with surety bonds before those that do not have them.

- Subcontractors are not required to file mechanics’ lines when there is a payment bond.

- Having surety bonds can help contractors’ businesses grow more by giving them more projects and opportunities because of the provided assistance and advice given by the surety bonds.

Contract Price

Premiums from surety bonds can vary from half a percent to three of the contract’s worth, depending on the project’s size and timetable and the hired contractor.

How do Surety Bonds Work?

The surety company protects the owner and everyone involved in the project with the assurance that the contractor will be able to finish the project successfully. Surety companies and bond producers have an evaluation process for contractors’ and subcontractors’ performance, which they have been doing for years.

Requirements: Before giving surety bonds, the surety company must be convinced that the contractor has the following:

- Good reference and reputation.

- Can meet all responsibilities and tasks assigned.

- Experience matching the contract requirements.

- Have complete tools and equipment to finish the work (or the ability to obtain them).

- Are stable financially or have the financial strength to support the desired work program.

- An excellent credit history.

- Should have a good relationship with banks and a line of credit.

What Happens if the Principal Fails to Complete The Agreement?

Failure for contractors is very common, and sometimes it can be unavoidable. In situations like that, the business owner should declare the contractors’ failures. The surety company then investigates before placing a claim. That secures the contractor if the owner untruthfully declares the contractor’s failures. But when the owner properly reports the faults, the bonds often state the options.

Who Buys the Bonds?

Bonds are stated explicitly in the contract, and the contractors should make sure they have those. The contractor generally has the premium amount, which is entirely payable during the execution of the bonds. Suppose the worth of their contract has been changed. In that case, the premium will be modified or adjusted according to the contract’s value.

Surety bonds used for contracts are one of the best investments for getting great, skilled, and qualified contractors. Surety bonds protect business owners from the costs if the principal fails. If everything goes well, the surety company will then release the contract.

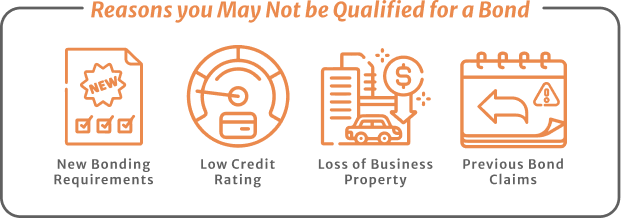

Why Don’t You Qualify for Surety Bonds?

People may find it difficult to qualify for the contract surety bond they require. Sometimes people have been bonded for years. However, they are struggling to qualify for a bond renewal. People don’t realize that there are reasons they may not be qualified for a bond, which might not even be their fault.

- One reason might be new bonding requirements developed by various government authorities. A previous financial downturn can significantly tighten the qualification standards. Unfortunately, this challenge cannot be avoided. Nevertheless, you can still improve the likelihood that you will be able to be eligible for the bond you need.

- If you have a low credit rating or a score that has dropped since you purchased your original surety bond, you may not be able to qualify for renewal or an initial grant. Increasing your credit score with a few points can give you an additional push towards authorization.

- Another problem that may obstruct your approval is a loss of business property. For instance, if your cash deposits have decreased since you bought your original bond, you may not be approved.

- Lastly, previous bond claims against you as a surety bondholder might also keep you from getting a bond. Fortunately, there are some steps you can take to achieve the qualification.

Prequalification Process for Surety Bonds

Every surety company has its own underwriting standards and requirements; however, there are shared fundamentals familiar to the underwriting of many surety organizations. Before a surety underwrites a bond, the contractor typically goes through a careful, rigorous, and thorough process, often known as prequalification.

The procedure takes time as the company collects information, answers questions the surety underwriter might have, and supports in verifying information. The surety has to be completely satisfied that a contractor can meet current and future financial obligations, has an excellent reputation, has experience meeting the demands of the projects to be undertaken, and has (or can easily obtain) the essential equipment to carry out the work. The surety also looks for contractors who run a well-managed, profitable business, keep promises, deal fairly, and carry out duties on time.

How to Secure a Surety Bond for Your Next Job

Professionals and customers alike usually have little knowledge about how to secure a surety bond. Even people required by law to buy surety bonds could get lost in the confusing process. Though the surety bond market is an integral part of the insurance business, little information is offered to advise individuals on how to secure a surety bond.

-

Determine how much time you have to get the surety bond

Most of the time, applicants wait until one week before their bond is due to apply for a surety bond. Even though surety bond providers have the capital to issue many bonds in just one business day, this would not be the usual protocol. Applicants need to comprehend that when surety providers issue bonds, they are doing lawfully binding contracts that offer security through a financial guarantee.

While underwriting high-risk or intricate bonds, surety providers will require more time to evaluate an applicant’s qualifications. That means that applicants must give surety providers sufficient time to do their job to the best of their ability. Including allowing time for physical delivery, as surety providers will charge extra fees to ship surety bonds express or overnight.

-

Collect information

That can affect your bond form application. Before you secure a surety bond, always ensure that all the useful personal information and company details are easily accessible. When considering you or your company as a great customer, surety providers will usually request:

- The exact business name as it appears on the business license.

- The exact penal sum (the bond amount).

- Social security numbers of all owners.

- Home addresses of all owners.

- All relevant personal and business financial records.

Surety bond producers would also inquire about your credit rating since it’s one of the most significant factors that might affect your surety bond cost. Your surety provider will look it up later during this process, but having a ballpark estimate early on permits the surety to give you an accurate cost estimate.

Find the Best Rate for Your Surety Bond

Those trying to secure a surety bond have two primary providers from which they can buy their bonds. An insurance company generally issued surety bonds, given they had the financial capacity to provide extensive economic guarantees. In the past decade, many specialized surety companies have come together to provide more comprehensive bonding services to principals who need to apply for a surety bond.

Finding a surety bond provider that will provide a competitive rate is much easier since most of today’s surety bond providers have a solid online presence. You can apply for surety bonds online and get a company selling price quote back in as little as one day. Just be sure you have the essential information at your disposal. You will get a more genuine price if you offer the surety provider the specific information in your initial request.

You can call our dedicated experts who only write bonds and can give an advice before you buy a surety bond.