As a new subcontractor, you might think that whoever you contract under will have a general liability insurance policy or some other insurance coverage that covers you. You may also think that the business owner’s policy covers you while you are on their site. Unfortunately, none of these options are true.

In fact, there are at least four types of subcontractor insurance that you will need to be safe if not others depending on your business and field in the construction industry.

General Liability Insurance

This type of insurance is the most common out of all policies that you can get. It covers all the bases and should be considered what your insurance policy builds off of. Commercial General Liability coverage is not contractor-specific or subcontractor specific, however, it’s a type of business insurance that is typically required to begin bidding on any project.

It’s important for business owners to know that they could end up paying more for the same type of coverage as compared to others in safer industries. This is because you will often face higher risks than other industries, especially if you work in a particularly high risk filed of construction such as skyscrapers versus parks and rec.

Commercial General Liability insurance can and usually does cover a few different things based on your needs, these include:

There are other things that General Liability Insurance will cover, however, many of those things are specific to general contractors or other types of business owners. Always remember, it’s best to call in an individual insurance agent for an insurance quote because unlike free quotes you get online, they will be able to customize it for exactly what you need and understand things a computer might not be able to, usually still for free!

Worker’s Compensation Insurance

This insurance is something that most states have requirements about no matter what industry you are in. You will, more than likely, also have some construction-specific laws that will need to be followed. This is to ensure that the high-risk industry you are in produces a safe workplace. Always purchase worker’s compensation from an insurance company after checking the state’s rules for exact insurance requirements.

It’s generally a good idea to get more than you need to meet the bare minimum should anything happen that could result in a lawsuit, however, what you choose will greatly affect the cost you will pay. In short, workers’ compensation insurance covers the medical costs you could have on your hand should an employee suffer injuries while on the job site or workplace.

Commercial Auto Insurance

Most if not all subcontractors will have a vehicle they use for the business if not a fleet that is used by the subcontractor’s employees. That’s why commercial auto insurance is a necessity. While your own insurance may cover your truck that you use for pleasure and business, it’s safer and more on the up and up to list any truck or vehicle you use for business on your auto insurance policy.

Should someone else is driving your vehicle, this more than surly the route you should go. This coverage is can help with quite a few things involving accidents from damage to the vehicles from an accident either on the road or on-site to damages caused by an employee driver to the site while on the job and even legal fees that result from dealing with these accidents.

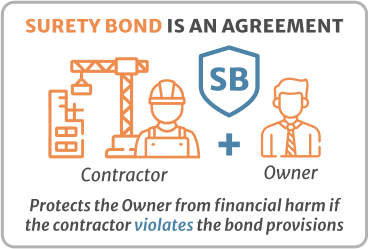

Surety Bond

Though not exactly insurance for you, this serves more like an insurance for the client that you work with. It protects your clients against liability and malpractice, very helpful for small business owners that normally couldn’t take the risk themselves. It helps to guarantee the project that you said you would complete, will, in fact, be completed within the stated terms.

For example, if you back out of a contract you said you would complete and you had a surety bond, the policy would cover the costs that the client needed to find a new contractor to complete your work left. Due to the unfortunate pervasiveness of this type of activity, these contractor-specific bonds are typically, if not always, required for bids and by clients.

As with any insurance or legal decision, make sure to get proper legal advice on what you need in your situation.

A Note About the Other Types of Construction Insurance

Though those are the most common types of insurance policies, there are a few others that should be mentioned when it comes to protecting you, the business owner, as well as the client from risk when running a construction subcontracting company. The first optional coverage, professional liability, is often called Errors and Omissions insurance.

This important insurance can cover mistakes that are made on the actual product made by your employees or independent contractors. It covers any potential lawsuits from those actions and helps you with the costs of defense. Most will consider this insurance to be required, but it can actually depend on whether your general liability policy provides this coverage.

Next, umbrella insurance. Completely optional, its coverage is as simple as it sounds, it helps cover the other things that your current policy covers. It can be used with a lower coverage policy to create a lower insurance cost if done correctly. The last optional overage, builder’s risk coverage, is an insurance that covers the loss of tools or other property you may own.

This insurance is almost always taken out as short-term coverage that covers an individual job at a time. It is highly recommended and sometimes even required by local codes or businesses, but sometimes it is up to the contractor to have it if they wish.

If you want to be risk free, get your insurance now!