Builder’s Risk policy extensions can be crucial for contractors, as far as risk management is concerned. And, in an industry that is projected to hit $1.2 trillion in economic activity by 2020, even minor property damages at the workplace can result in severe financial loss. This, in turn, can cause a delay, halt your entire construction project, and cause serious financial implications.

For contractors, tailored Builder’s Risk insurance coverage goes a long way to protect your business against financial loss. As a result, a common Builder’s Risk insurance policy may cover property damage from causes such as fire and theft. But, are there Builder’s Risk policy extensions that you should explore? By the end of this guide, you’ll be familiar with common extensions covered under the Builder’s Risk policy.

What Is Builder’s Risk Insurance?

Builder’s Risk Insurance, especially designed, it will provide coverage for the damages done to structures and buildings under construction or renovation. As a result, other than covering the costs of construction, your policy also covers tools and equipment used at the construction site.

Builder’s Risk Insurance is also a Course of Construction insurance policy.

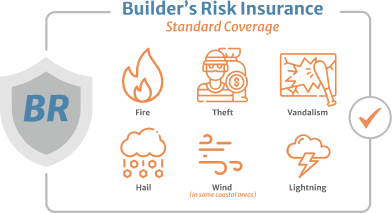

Standard Builder’s Risk Coverage

Your Builder’s Risk policy provides coverage to a building against damage or destruction from a wide variety of covered risks. These risks include:

- Fire

- Theft

- Vandalism

- Hail

- Wind (In some coastal areas)

- Lightning

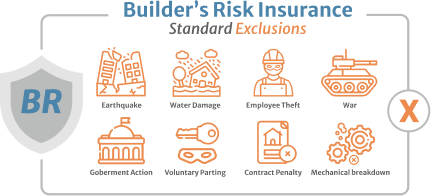

Builder’s Risk Limitations

Before you purchase your Builder’s Risk insurance policy, however, it is important to familiarize yourself with its limitations and the exclusions from the policy. As standard, most common exclusions are:

- Earthquake

- Water Damage

- Employee Theft

- War

- Government Action

- Voluntary Parting

- Contract Penalty

- Mechanical Breakdown

Also, your Builder’s Risk policy excludes damages due to faulty design, workmanship, planning or materials. Bear in mind, such risks are covered under professional liability coverage.

Who Needs Builder’s Risk Insurance?

In most cases, both homeowners and general contractors should have Builder’s Risk insurance while working on a construction project. However, lending institutions require general contractors to have coverage before they obtain a loan with them. Moreover, this serves the purpose of protecting the lender in case of a financial loss. Moreover, each project is different and will need its own Builder’s Risk policy extensions.

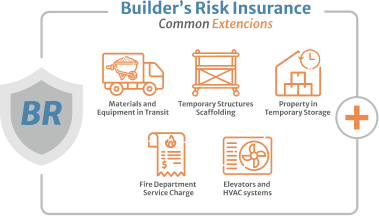

Common Builder’s Risk Policy Extensions

In order to make sure your business and project is fully covered, you can add extensions to your policy. Common Builder’s Risk policy extensions include:

- Protection for materials and equipment while in transit.

- Coverage extension to temporary structures scaffolding.

- Property in temporary storage.

- Fire department service charge.

- Properties such as elevators and HVAC systems.

How Much Does Builder’s Risk Insurance Cost?

The cost of your Builder’s Risk insurance policy depends on several factors. These include the type of construction, length of the project, and exclusions on the policy. However, on average, the quote of the policy ranges between 1% to 5% of the total cost of the construction project.

[/et_pb_text][et_pb_text admin_label=”Policy Terms” _builder_version=”4.18.0″ _module_preset=”default” global_colors_info=”{}”]

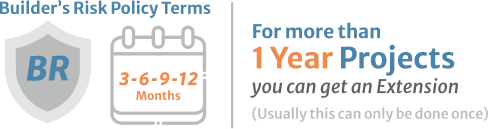

Policy Terms

Your Builder’s Risk insurance policy is written in quarterly, semi-annually, or annual terms. However, if your project takes longer than one year, it is possible to have an extension, but usually, this can only be done once. Nonetheless, contractors should check this information with their insurers to know more about available policy terms.

Understanding how Builder’s Risk Policy extensions can be confusing. Moreover, we offer help if you need any assistance.