Vacant buildings are prime targets for vandalism and subject to all the risks of occupied structures. While occupied buildings have many eyes to watch for potential hazards or security risks, unoccupied structures are inherently more risky as there is no one around to spot trouble. This risk also encompasses unlawful intruders into the premises that could potentially sue the property owner for any injuries sustained while trespassing in an unoccupied structure.

Home insurance policies have vacancy clause that will still cover unoccupied building. This is applicable when a family is away for vacation. However this is only for limited period of time, which is 30-60 days. This means, if the house has been vacant for more than 60 consecutive days, any property damage or bodily injury that occurred in the premise are no longer covered. So when a family leaves home for a long vacation, building is up for renovation, still searching of qualified tenant to occupy, or maybe it’s up for sale, vacant building insurance should be highly considered.

What are primarily covered in a vacant insurance?

- Building

– Insures property if something happens to it by covered cause of loss like fire. - Personal property

– Coverage from theft and property damage. - Vandalism and Glass Breakage

– Just like what we always see in the movies, intruders like to do it a lot. - Liability

– Unoccupied structures are inviting to trespassers. But if they get hurt while within the premise, owners can still be sued. Liability covers defense costs if that happens. It also pays medical expenses up to a limit without regard to fault to discourage people who gut hurt from filing a lawsuit.

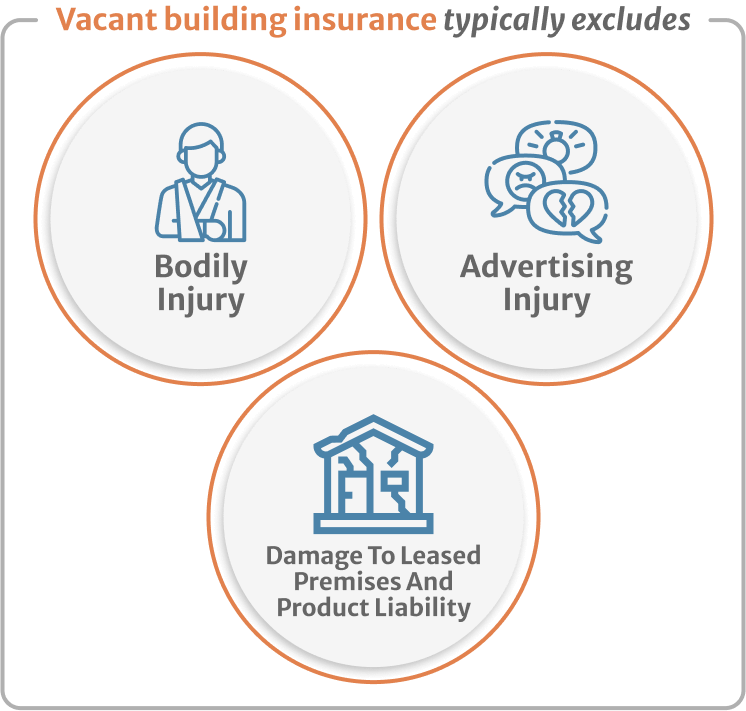

What is excluded from vacant building insurance policy?

Unlike regular general liability coverage, personal and advertising injury, damage to rented premises and products liability are usually excluded. A lot of clients asking for vacant building insurance have asked why are these specifically excluded? They are excluded for the main reason that these coverage won’t even be applicable on a vacant building.

For example, advertising and personal injury protects insured from lawsuit against misappropriation of advertising idea, slander, libel, malicious prosecution, etc. And a vacant building doesn’t need protection from these. Products-completed operations also does not apply as it provides liability caused by the insured’s product (if insured is making and selling pie that caused food poisoning) or business operation (e.g. roofer that didn’t do his job well causing water damage from the leak making the homeowner file a claim against roofer’s GL insurance).

Lastly, fire damage under general liability refers to a tenant’s liability for damage by fire to the rented premises, which in the case of a vacant building is not applicable as there should be no tenant living in premise in the first place. If the building is burned to the ground (God forbids), insurance will cover replacement under property/building coverage.

What can be added to vacant building insurance policy?

The following coverage can also be added on a vacant building policy:

- Equipment breakdown

– Mechanical breakdown and electrical arcing.

– Loss or damage to hot water boilers and steam equipment.

– Steam explosion of boilers, piping, engines and turbines. - Terrorism coverage

– Under the Terrorism Risk Insurance Act, every insured has the right to purchase insurance coverage for losses arising out of acts of terrorism.