Workers Compensation Audit: What Contractors Need to Know

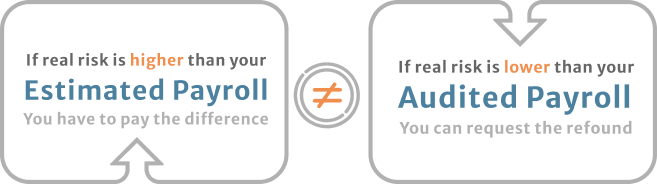

A workers compensation audit is not a penalty. It is a standard end-of-year reconciliation that every workers comp policyholder goes through. The premium charged at the start of the policy was based on estimated payroll. The audit confirms what the actual payroll was and adjusts the cost accordingly. If payroll came in lower than estimated, the carrier owes a refund. If it came in higher, the business owes the difference.

Farmer Brown walks contractors through this process across all 50 states. Here is what to expect, what documents to have ready, and what the common mistakes are.

Why workers’ compensation audits happen every year

When a workers comp policy is written, the carrier estimates annual payroll to calculate the starting premium. That estimate is a projection, not a final number. Business conditions change throughout the year: crews expand, projects slow down, subcontractors come and go. The actual payroll at year end rarely matches the figure used at policy inception.

The audit recalculates the earned premium based on real payroll figures and the actual class codes for the work performed. If the business grew and payroll was higher than estimated, there is an additional premium due. If payroll was lower, the carrier issues a credit or refund.

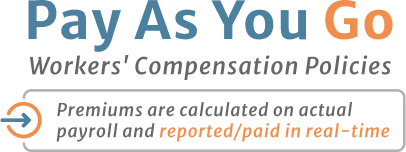

Pay-as-you-go workers comp policies reduce the size of audit adjustments by calculating premiums against actual payroll each pay period in real time rather than estimating at the start. The final audit adjustment on a pay-as-you-go policy is typically smaller than on a traditional estimated direct bill program.

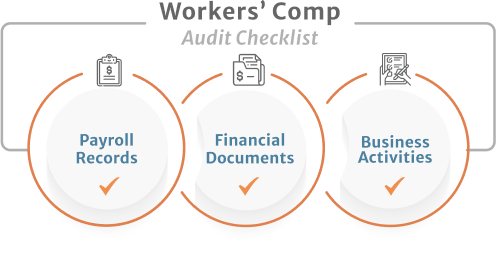

Documents required for a workers compensation audit

| Document category | Specific records needed |

|---|---|

| Payroll records | Payroll journal, checkbook, individual earnings records, federal 941 tax returns, state unemployment tax returns |

| Overtime records | Separate payroll records showing overtime wages broken out from regular pay |

| Financial documents | Profit and loss statements, bank statements, business tax returns |

| Subcontractor records | Certificates of insurance, signed agreements, invoices showing labor and materials separated |

| Business activity records | Description of business operations and employee job classifications for the policy period |

Having these organized before the auditor contacts you shortens the process significantly. Auditors work with what they are given. If documentation is incomplete, they make their own estimates, and those estimates are rarely in the policyholder’s favor.

How to prepare for a workers compensation audit

Organize documents before the auditor asks for them

Pull the records for the full insurance term before the audit is scheduled. The specific documents an auditor requests can vary by carrier and state, but payroll records and subcontractor certificates are required in almost every audit. Having them ready prevents delays and eliminates the back-and-forth that slows the process down.

Review and update job descriptions for every employee

Workers comp premium is calculated partly by what each employee does, not just what they are paid. A laborer doing ground-level finish work is in a different class code than one doing structural framing at height. Class codes carry different rates, and the auditor will verify that each employee’s classification matches their actual duties.

If job descriptions have not been updated in the past year, update them before the audit. Vague or outdated descriptions give the auditor room to assign a higher-rate class code than the work actually warrants.

Only provide what the auditor requests

Providing more documentation than the auditor asked for creates unnecessary work for both sides and can introduce information that raises questions. Provide exactly what is requested. If something is unclear, ask before submitting.

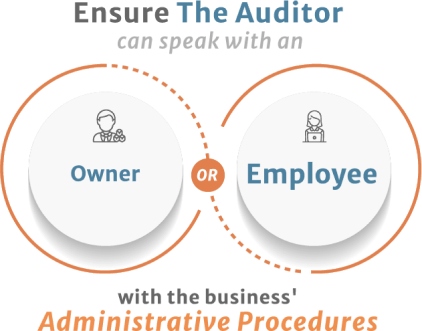

Make sure an owner or someone familiar with the business’s day-to-day operations is available to speak with the auditor. Someone who can answer questions about employee responsibilities and project types on the spot prevents misclassification.

Review the audit findings before signing anything

Before signing off on the completed audit, read through the documentation the auditor produced. If any employee classifications look wrong or payroll figures do not match your records, raise the question before signing. Signed audit records are harder to dispute after the fact. Once an audit is complete, policyholders have up to three years to formally dispute the findings, but resolving issues before signing is simpler.

What happens when estimated and audited payroll figures do not match

| Scenario | Result |

|---|---|

| Actual payroll matches the estimate | No adjustment, no additional premium due |

| Actual payroll was lower than estimated | Carrier issues a refund or credit toward the next policy |

| Actual payroll was higher than estimated | Business owes additional premium to the carrier |

| Subcontractor certificates were missing | Subcontractor payroll may be added to your own, increasing premium |

| Employees were misclassified | Auditor reassigns class codes, which can raise or lower the adjustment |

The Final Audit Statement the carrier sends after the audit details every adjustment, whether premium is owed or credited, and how the auditor arrived at the final figures. Review it line by line. Errors in class code assignment or payroll allocation are not uncommon, and they are correctable.

How subcontractors affect your workers comp audit

Subcontractors are one of the most common sources of audit surprises for contractors. If a subcontractor working on your projects does not carry their own workers compensation insurance, the carrier will treat the wages paid to that subcontractor as part of your own payroll. That increases your premium.

The fix is straightforward: collect certificates of insurance from every subcontractor before they start work. Keep current copies on file throughout the year. At audit time, those certificates document that the subcontractor carried their own coverage, and those wages stay off your payroll calculation.

Keep all subcontractor agreements and invoices, and make sure labor costs and material costs are broken out separately. Auditors need to see the labor portion clearly to assign it correctly.

How overtime pay is handled in a workers comp audit

Overtime wages are frequently included in the audit total because employers do not always maintain separate records showing which portion of wages was overtime. That matters because most states allow overtime pay above the regular rate to be excluded from workers comp payroll calculations.

To capture that exclusion, the business needs to maintain payroll records that clearly separate regular wages from overtime premium pay. Without that documentation, the auditor includes the full overtime amount in the payroll figure. The requirement is that the employer pay overtime at the employee’s standard hourly rate as the basis for the calculation, with the overtime premium portion separately documented.

Check your state’s specific rules. Some states calculate the exclusion differently.

What happens if you do not complete the workers comp audit

Ignoring a workers comp audit has direct financial consequences. Failing to comply with the audit terms violates the policy contract. The carrier can issue a non-compliance premium, which is typically set significantly higher than any realistic audit adjustment would have been. In most cases, the carrier assumes maximum payroll exposure and charges accordingly.

Some carriers will cancel the policy for non-compliance. A canceled workers comp policy creates problems beyond the audit itself: it goes on record and can make coverage harder to obtain at standard rates going forward.

If the audit timeline becomes difficult to meet, contact the carrier directly. Most auditors allow extension periods for businesses that communicate proactively.

Frequently asked questions about workers comp audits

How long does a workers comp audit take?

Most audits for small to mid-size contractors are completed within a few days to a couple of weeks depending on how organized the records are. A business with complete, well-organized payroll records and current subcontractor certificates moves through the process faster.

Can I dispute audit findings I disagree with?

Yes. Policyholders have up to three years after the audit is completed to formally dispute the findings. The most common grounds for dispute are incorrect employee classification, misallocation of subcontractor payroll, and overtime calculation errors.

What is a pay-as-you-go workers comp policy?

A pay-as-you-go policy calculates workers comp premium against actual payroll each pay period rather than estimating at the start of the year. Because the premium tracks real payroll in real time, the end-of-year audit adjustment is typically much smaller than on a traditional estimated program.

Does workers comp cover independent contractors?

Generally no. Workers comp covers employees, not independent contractors. But if a subcontractor is later determined to be an employee under state law, the coverage question gets complicated. The safest approach is to require every subcontractor to carry their own workers comp policy and provide a certificate of insurance.