Did you know that nearly 44% of small businesses do not have liability coverage?

This is riskier for some businesses than for others. General contractors are one business type that definitely falls into the must-have group when it comes to liability coverage. If you are in the contracting industry, you must take out insurance to protect your business.

This is because general contractor work comes with a high risk of liability. If your businesses causes damage to a client’s property, you are the one responsible for paying. If a client of yours is injured thanks to your presence on their property or your work, you are also liable for this.

Depending on the level of damage or injury, these types of claims could spell disaster for your business. If you don’t have the funds to pay, you could face lawsuits and bankruptcy. If you have the funds, the scenario isn’t much better because you might have to hand out a sizable sum that you could have invested in your business.

Fortunately, general contractors’ insurance protects you from these hazardous scenarios. If you want to protect your business, gain peace of mind, and attract more customers, then contractor insurance is a must.

What to find out why? Keep reading as we outline all the ways that contractors’ liability insurance can safeguard your business and why this is so essential.

1. General Contractors Insurance Protects Your Business From Going Bankrupt

If there is one overarching reason why you need general contractors’ insurance, it’s that it can protect you from bankruptcy. As mentioned above, if a client or third party experiences bodily harm or property damage as a result of your services you could be in for a big bill.

Depending on how high the amount is, you or your business might face bankruptcy as a result. Bankruptcy not only means the end of your business, but it can also have some other far-reaching effects.

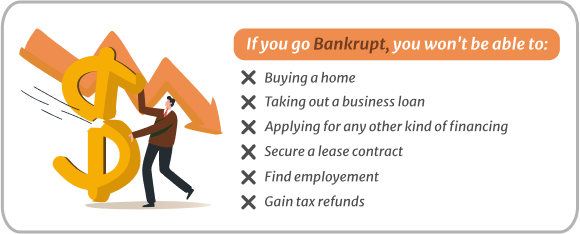

If you are a sole proprietor, you take sole responsibility for your business’s debts. Having to file for bankruptcy will have dire effects on your credit record. This can prevent you from buying a home, taking out a business loan, or applying for any other kind of financing. What’s more, filing for bankruptcy can also make it difficult to secure a lease contract, find employment, gain tax refunds, and more.

As you can see, bankruptcy is something that most businesses and sole proprietors should avoid at all costs.

At the same time, even if you have the funds to avoid bankruptcy and pay any claims for damages, this will still most likely be highly detrimental to both you and your business.

2. It Also Protects You From Law Suits

Besides safeguarding you from bankruptcy, contractors’ liability insurance can also protect your business from lawsuits. If your business does not have contractor insurance it will be up to you to either pay or contest any liability claims third-party levels against you.

If you are in the wrong, then, as mentioned above, you will need to pay up for the damages.

However, what happens if you don’t think you are in the wrong?

If you feel that an unfair claim has been leveled at you, you can try refusing to meet the demands made on you. However, if the third-party wishes to continue, they can then take the matter to court. Even if the court rules that you were not-at-fault, this is still usually a costly process.

Beating a liability claim on your own can be tough. In most cases, you will need to hire a lawyer to defend you. Their fees, combined with any other court costs, can quickly mount up. If you end up losing the case, you will need to pay these costs as well as the claim amount.

Fortunately, if you take out general contractors’ insurance, you can avoid all of this. When you’re covered by contractors’ liability insurance, the insurance company will decide whether or not any claims are valid. Insurance providers have their own legal teams at hand and are skilled at dealing with third party claims.

If the claim is valid and covered by your liability insurance coverage—the third party will be paid out, and you won’t have to face going to court.

3. It’s the Law In Some States

General liability insurance for contractors not only protects your business; in some states, it’s also the law.

Depending on where you live, your state might require proof of general contractors’ insurance before they will issue you with a license. All contractors must have a business license, and some need also to have a contractor’s license for specialty work.

Not sure what the laws are in your state? If you’re unclear what they are, you can look up your state’s requirements here.

If your state requires general liability insurance, you should take out coverage as soon as possible to be able to apply for your business or contractor’s license. If your state does not require general contractors’ insurance, you should still look at applying for coverage, thanks to all the ways it can protect your business.

We do the work for you! quote your insurance now!

4. Contractors Liability Insurance Protects You From All Third-Party Claims

Did you know that general liability insurance for contractors protects you from most third-party claims, not just those from your client? Most general liability policies will cover you for damage or harm done to other parties that are also present on the property where you’re working.

This means that if there are other contractors working on the job site or people other than your client on the property, your insurance will cover them too. If injury or damage to property is caused to any of these parties as a result of your actions, your contractors’ general liability insurance will likely cover it.

For instance, say one of your employees was removing nails from a beam, and another contractor’s vehicle pulls up. By a stroke of bad luck, one of the nails is lying upright in the driveway, and the contractor’s truck happens to drive over it, resulting in a puncture. If the cost of repairing or replacing the tire is more than your deductible, the insurance company will cover the excess.

In a different scenario, say a visitor trips over a power lead of yours and breaks their wrist. Because they are a third party on your job site, your contractor insurance should cover any expenses should the third party wish to make a claim.

If you are thinking, “But what are the chances of having to ever meet a claim like this?” take note that according to statistics, there are 71% more non-fatal injuries on construction sites than in any other industry.

If you are doing work on a client’s property, you are essentially turning it into a construction site. During this time, anybody who is moving through the area has a heightened risk of injury.

5. It Also Covers Injury and Damage Occurring From Completed Projects

Another way that contractors’ liability insurance will protect your business is that it covers you for damage or injury resulting from projects you have already completed.

Say, for instance, you install a handrail for a client’s staircase. A week after installation, the handrail comes loose, a family member grasps it, falls and breaks their arm, and the rail goes flying and cracks a glass sliding door.

If you have general liability insurance for independent contractors, this should cover any costs claimed by the client.

Take note that general liability coverage will not cover projects that the client is simply dissatisfied with. However, if a project is the direct cause of damage or injury, you should be able to claim the associated costs from your liability coverage.

6. Advertising Claims

False advertising claims are on the rise, and most businesses would do well to protect themselves from these. Although it is not highly likely as a general contractor that you would have a false advertising claim laid against you, the possibility is always there. General liability policies often provide coverage for false advertising claims.

Another type of advertising claim that can be hard to combat are accusations that your business is duplicating another similar business’s marketing tactics. If you have contractors’ liability insurance, this will cover you against any damages through these types of claims.

Some general liability insurance will even provide cover for cases of slander.

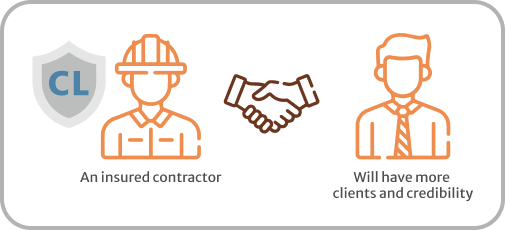

7. Having Contractor Insurance Protects Your Reputation and Establishes Trust

Besides protecting your business financially, having contractor insurance also safeguards its reputation and establishes trust with potential clients.

If your contractor business does not hold insurance, it’s easy for clients to see you as an unprofessional operation. On the other hand, if you have adequate liability coverage, this shows potential clients that yours is a professionally run business.

What’s more, it also reassures clients that should there be any damage to their property from your services; they won’t have to foot the bill.

If you take a moment to look at any of the online guides on how to choose a good contractor, most of them will say go for licensed and bonded ones. If your contractor business is insured for general liability, clients will immediately see you as a cut above any that are not insured.

According to estimates, there are currently over 700,000 construction companies in the US. Depending on your location, the competition might be stiff, which means you need to do everything you can to stand out from the pack. Getting general liability insurance for independent contractors is one way you can accomplish this overnight.

Once you have been approved for your general contractors’ insurance, make sure you advertise this on your website and marketing materials.

8. An Add-on Can Also Insure Your Equipment

One thing that contractors’ liability insurance does not cover is equipment. If your tools or equipment breaks, you will not be able to claim for this under general liability coverage.

However, the good news is that you can easily insure your tools and equipment as well by purchasing an add-on. Depending on your insurance provider, you may find that an add-on is cheaper than taking out separate cover for your equipment.

Opting for an equipment coverage add-on can save you money in the long run, and it can also guarantee that your business’s operations never have to suffer because you can’t afford to replace a malfunctioning piece of equipment.

Entrusting your equipment to employees often comes with the risk of breakages and decreased lifespans. Considering that tools and equipment are essential to most contractors’ businesses, insuring them is usually a smart option.

Protect Your Business Today With General Contractors’ Insurance

General contractors’ insurance is not just a nice-to-have. In some states, it’s the law. However, regardless of the state you live in, general liability insurance for contractors can protect your business from claims laid against you due to property damage or accidents.

Sometimes these types of accidents are unavoidable, so don’t assume that just because you run a tight ship, you don’t need coverage.

Ready to start protecting your business with contractors’ liability insurance? If so, you have come to the right place. Here at Farmer Brown, it’s our business to connect you with the right insurance offers to suit your individual requirements.

To get started, all you have to do is fill us in on your needs by telling us about your business. Once we know what your unique requirements are, we will match you up with the optimum policy. From here, you can choose between multiple financing and payment options.

You will then be issued with your certificate of insurance and be able to access our 24/7 support whenever you need it. Simply fill out this quick form for a free quote, or call us today!